All it takes is a few clicks.

Written by: Chloe Lomax, Senior Writer at The Hartford

Reviewed by: Gene Marks, CPA, Author & Small Business Owner

When you get business insurance, you’ll choose from either a claims-made or occurrence policy. What’s the difference between a claims-made vs. occurrence policy? Well first, know that it directly affects the kind of coverage you have, so it’s important to know how they work.

At The Hartford, we offer both, and we’re here to help you learn the difference between claims-made vs. occurrence policies so you can make the right decision for your business.

What Is a Claims-Made Policy?

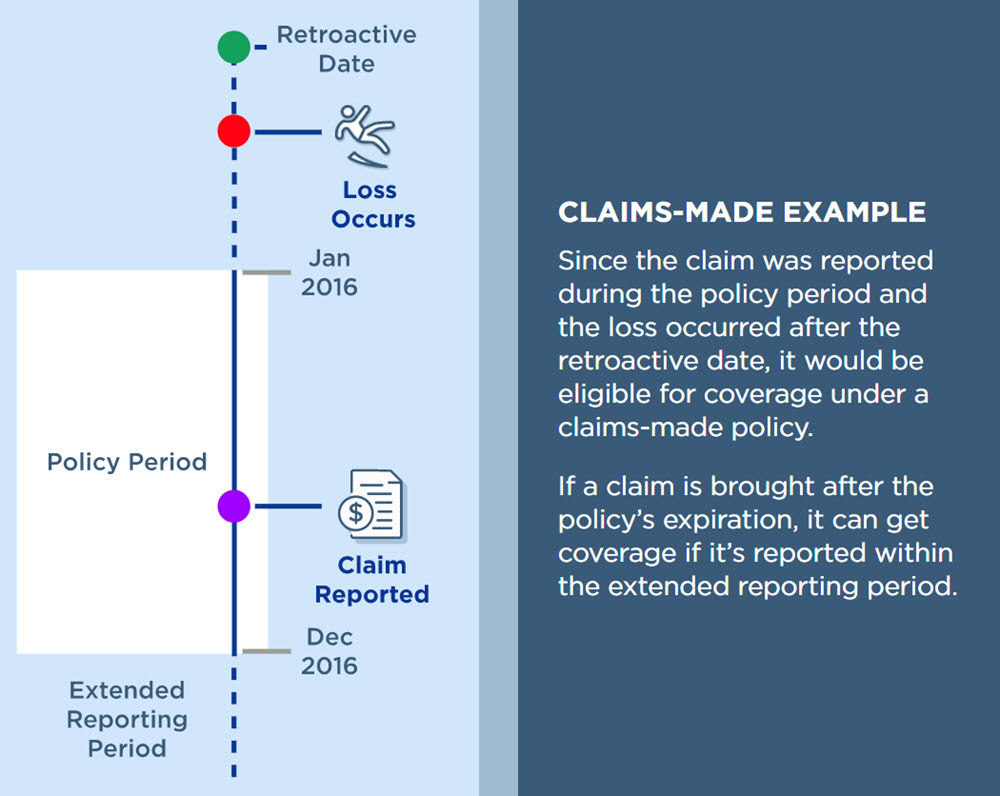

Insurance companies commonly write policies on a claims-made form. This means your insurer helps cover claims filed during your policy period.

There are two features of a claims-made policy that can affect coverage:

Retroactive date: Your policy provides coverage if an incident occurs on or after a specified date. Let’s say you have professional liability insurance written on a claims-made policy. Your coverage starts in January 2021 and has a November 2019 retroactive date. If your client sues you in February 2021 for an event that occurred in December 2019, your insurer can help cover the claim because it happened after your retroactive date and the claim got reported during your policy period.

Extended reporting period: This helps cover claims made during a specified time after your policy expires. Generally, it lasts between 30 and 60 days. So, if your policy expires in December 2021 and you have a 60-day extended reporting period, your insurer can help cover claims reported in this window. This is also known as tail coverage.

It's important to remember that a claims-made policy covers your business only if the claim is:

- Filed during your policy period or within your extended reporting period

- For a loss occurring on or after your retroactive date

For losses or incidents that happened before your policy started, your insurance company won’t provide coverage. Instead, you’ll need prior acts coverage to help with these kinds of claims. With prior acts coverage and tail coverage, you may have more peace of mind since your business will have more protection.

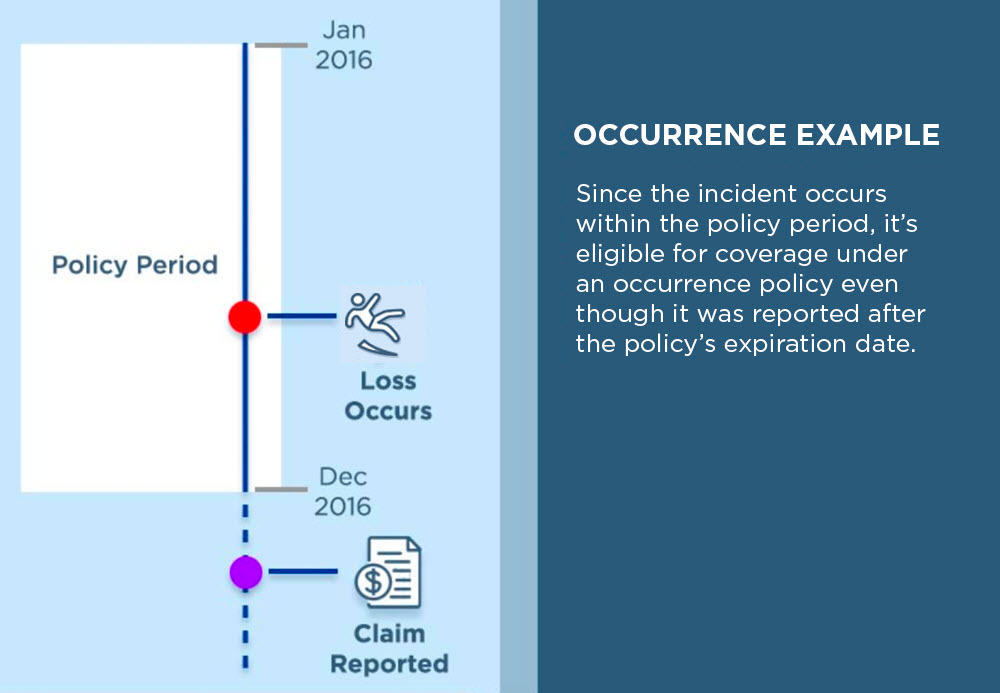

What Is an Occurrence Insurance Policy?

An occurrence policy provides coverage for incidents that happen during your policy period, regardless of when you file a claim. These policies can be more expensive than a claims-made policy because of how long coverage applies.

Let’s say your business has commercial general liability insurance coverage written on an occurrence form. During your policy period, your customer breaks their arm after a slip and fall in your business. However, they don’t report the incident until a year after your policy expires. Because they got hurt while your policy was in effect, the claim can still get coverage.

Do I Need Tail Coverage If I Have an Occurrence Policy?

No, you don’t need tail coverage if you have an occurrence policy. That’s because you’ll get coverage for a claim if the incident occurred during the policy period – even if you’re reporting claims after your policy’s expiration date. So, tail coverage isn’t needed.

Claims-Made vs. Occurrence Policy

To determine whether you need a claims-made policy or an occurrence policy, you have to decide which one makes the most sense for your business. Since every business is unique, what works for one company may not work for yours.

Is Occurrence or Claims-Made Better?

There’s not an advantage to having claims-made or occurrence coverage. You’ll likely pay more for insurance written on an occurrence form. Be aware that insurers may write coverages on a certain type of policy. For example, we only write our business liability coverage on an occurrence policy. Policies that we offer on a claims-made coverage aren’t available on an occurrence policy.

Claims-Made and Occurrence Policies From The Hartford

It’s important to understand how your insurance policies cover claims. So, if the unexpected happens, you’ll know you have the protection you need. We’re an experienced insurance company and are proud to put our customers first. Our team of specialists are here to help in any way they can.

Whether you have questions about what business insurance is, when to get business insurance or how much business insurance costs, we’ve got your back.

Get a business insurance quote today and see how we can help protect you and your company.

Last Updated: September 21, 2023

Additional disclosures below.