All it takes is a few clicks.

Written by: Chloe Lomax, Senior Writer at The Hartford

Reviewed by: Gene Marks, CPA, Author & Small Business Owner

How Are Workers' Compensation Insurance Premiums Usually Calculated?

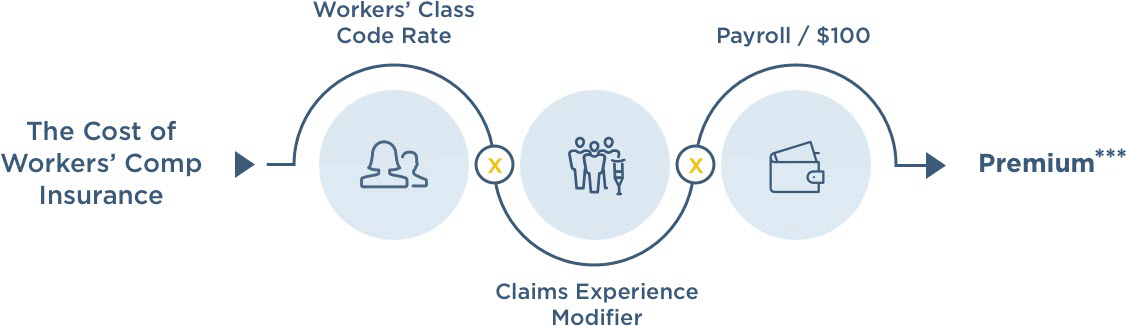

You can estimate your workers’ compensation insurance costs through this formula:

Each state has its own classification code depending on the type of work performed by your employees. The National Council on Compensation Insurance (NCCI) assigns these codes.

Your state may also determine your business’ unique experience by comparing your company to others in your industry.

Your business’ payroll gets multiplied by a rate that matches the class code. Each class code has a rate per $100.

Together, these items help determine workers’ compensation rates.

How Is Workers' Comp Calculated?

How much workers' comp pays for an injured employee is based on a simple formula or workers' comp calculator, using their average weekly wage on the date of the injury. Watch the video to learn about how workers’ comp is calculated.

How Much Does Workers’ Comp Pay?

No matter what type of business you run, on-the-job injuries or illnesses can happen. This is where workers’ compensation insurance can step in and give your employees important benefits. An injured or ill employee can file a workers’ compensation claim and receive weekly payments to cover medical bills or lost wages. This coverage is also known as workers’ comp insurance and workman’s compensation. Remember, this coverage won’t help if your employee gets a personal injury that’s not related to their work. But it can help protect your business from liability if you’re sued by an employee for a work injury.

No matter what type of business you run, on-the-job injuries or illnesses can happen. This is where workers’ compensation insurance can step in and give your employees important benefits. An injured or ill employee can file a workers’ compensation claim and receive weekly payments to cover medical bills or lost wages. This coverage is also known as workers’ comp insurance and workman’s compensation. Remember, this coverage won’t help if your employee gets a personal injury that’s not related to their work. But it can help protect your business from liability if you’re sued by an employee for a work injury.

Average Weekly Wage

Small business workers’ compensation benefits give your employees a percentage of their average weekly wage. However, the weekly payment amounts they receive will depend on regulations from your state workers’ compensation insurance.

This example can help you learn how to calculate your employees’ average weekly wage:

Your full-time employee made $50,000 last year after working for 242 days. If you divide $50,000 by 242, their average daily wage is $206.61.

Next, multiply $206.61 by 260 (the number of days a full-time employee would work in a year). That should equal $53,718.60.

Finally, divide $53,718.60 by 52 (the number of weeks in a year), to get your employee’s average weekly wage of $1,033.05.

Partial vs Total Disability

The weekly amount your employees receive is also based on the type of injury or illness they have. If they’re partially or totally disabled, they’ll get different benefits than someone with a temporary injury. In fact, a totally disabled employee will typically get 60% or 2/3 of their average weekly wage. Each state also has a maximum weekly rate, so you’ll want to make sure you understand the rules and benefit amount for your state.

If you’re wondering how long workers’ comp lasts, that also varies. Generally, the more severe a work-related injury or illness is, the longer payments last. If you expect your employee to need future medical treatment beyond regular workers’ comp payments, you may want to advise them to talk to a lawyer for legal advice.

What Are The Premium Rate Factors?

So, how is workers’ comp calculated? To figure out workers’ comp premiums, you’ll first need to understand the factors that influence them, such as:

So, how is workers’ comp calculated? To figure out workers’ comp premiums, you’ll first need to understand the factors that influence them, such as:

- Workers’ class codes

- Number of employees

- Payroll

- Claims history

Each state has its own classification code depending on the type of work performed by your employees. The National Council on Compensation Insurance (NCCI) assigns these codes.

Your state may also determine your business’ unique experience mod by comparing your company to others in your industry.

Your business’ payroll gets multiplied by a rate that matches the class code. Each class code has a rate per $100.

Together, these items help determine workers’ comp insurance cost.

Learn More About Workers’ Compensation From The Hartford

Contacting insurance companies to learn how to get workers’ comp insurance or filing a claim can be a hassle. We can help make workers’ compensation cases simple.

In fact, small businesses have relied on us for over 200 years. Our team can help you get the workers’ compensation coverage you need to protect your business and employees. You can also learn more by looking through our workers’ compensation definition and FAQs page.

Last Updated: July 23, 2026

*** This is a simplified calculation for educational purposes only. Actual premium calculations can be more complex. Experience mods are subject to state requirements and do not apply to every policy.

Additional disclosures below.