All it takes is a few clicks.

Do You Need Workers’ Compensation for Independent Contractors?

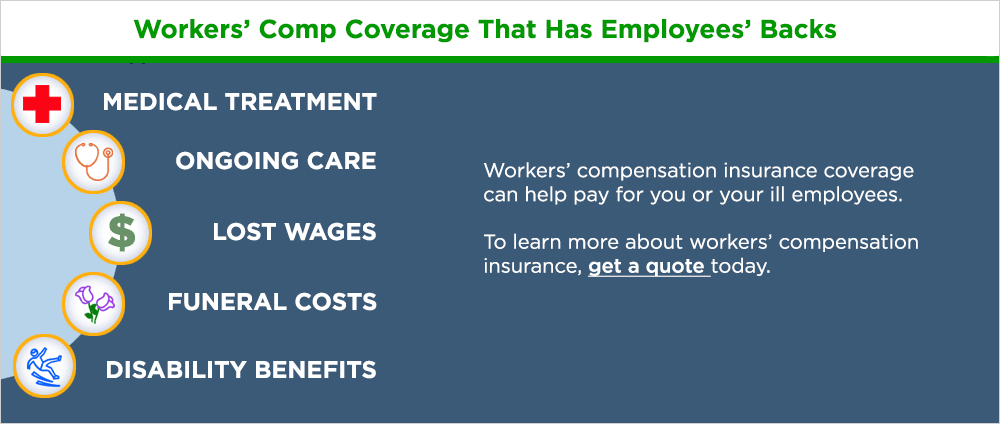

Workers’ compensation insurance coverage provides benefits to your employees if they experience a work-related injury or sickness. Also known as workers’ comp or workman’s comp, this coverage helps cover medical costs. It can also help replace some lost wages. When an employee accepts workers’ comp benefits, he or she also loses the ability to sue your business for damages.

Although typically used for employer-to-employee relationships, it also applies to independent contractors. For an independent contractor, workers’ compensation insurance can help protect them from work-related injuries or illnesses.

Do You Need Workers’ Comp If You Are Self-Employed?

Nearly every state requires employers to offer workers’ comp insurance to employees. States require different types of employees to be covered by workers’ comp. If you’re a sole proprietor, your state may not require buying workers’ comp insurance for self-employed businesses. If you work as a general contractor or a subcontractor, you may have to buy workers’ comp insurance if the contract you signed requires it.

Nearly every state requires employers to offer workers’ comp insurance to employees. States require different types of employees to be covered by workers’ comp. If you’re a sole proprietor, your state may not require buying workers’ comp insurance for self-employed businesses. If you work as a general contractor or a subcontractor, you may have to buy workers’ comp insurance if the contract you signed requires it.

A health insurance policy usually excludes work-related incidents. Say you’re self-employed and you have health insurance. While you’re working, you lift a heavy box and throw out your back. Your health insurance may not cover your medical costs because it’s a work-related injury. This means you’re responsible for the fees and costs related to your injury. The same scenario applies if you’re an independent contractor. Learn more about health insurance vs workers’ compensation.

That’s why it’s important to have workers’ comp coverage – even if you have health insurance. It can help prevent you from going through a financially ruinous situation.

Do 1099 Employees Need Workers’ Comp?

Workers’ compensation insurance usually does not cover 1099 independent contractors because they are considered self-employed. In most cases, contractors are responsible for purchasing their own coverage, though some states or industries require businesses to provide it. If a worker is misclassified as a contractor but functions like an employee, the hiring business may be liable for coverage, penalties and unpaid benefits.

While workers’ compensation can help provide benefits to cover work-related injuries and illnesses, you may still be at high-risk to other liabilities. Consider other types of insurance that can help protect self-employed and independent contractors. These coverages include:

General liability insurance helps protect your business from different claims. These include bodily injury, personal and advertising injury, and property damage.

Errors and omissions insurance helps protect you and your business when a mistake is made in the professional services provided to a customer.

Commercial auto insurance helps protect you if you’re using a vehicle for business purposes and are found at fault of a car accident. If there is property damage or bodily injuries, this can help cover the costs.

Without these other coverages, you may be responsible for the costs. The costs of damages can be extensive and enough to sink a small business or company you worked hard to build.

Does Workers’ Comp Cover Part-Time Employees?

What Is the Difference Between a Self-Employed and Independent Contractor?

If you have an employee for your business, you went through the process to hire them. And when they’re paid, your business withholds and pays various taxes. These taxes include income and Medicare. Self-employed or independent contractors don't have their pay withheld. Instead, they're responsible for paying a self-employment tax.

Early in the year, employees, self-employed and independent contractors receive tax forms. These forms show how much they got paid and how much they paid in taxes during the previous tax year. Workers that receive a W-2 tax form are considered employees. Workers that receive a 1099 are typically considered independent contractors.

Volunteers Covered Under Workers’ Compensation

Are Volunteers Covered Under Workers’ Compensation in New York?

Unpaid volunteers doing charitable work for a nonprofit organization aren’t considered employees. So, they don’t have to be covered by a New York workers’ compensation policy.1 If volunteers get compensated, they may have to be covered by a workers’ compensation policy. Compensation doesn’t just include pay or a stipend. It can include room and board and other perks that have monetary value. Money given to offset expenses made while volunteering is not considered a stipend.

In New York, a for-profit business cannot have volunteers. The state considers these individuals as employees. This means they should receive W-2s. They also have to be covered by workers’ comp insurance.2

Volunteer firefighters and ambulance workers in New York receive benefits for death or injuries sustained while in the line of duty. These benefits are provided under the Volunteer Firefighters’ Benefit Law and Volunteer Ambulance Workers’ Benefit Law.3

Are Volunteers Covered Under Workers’ Compensation in Florida?

Workers’ compensation benefits in Florida are typically only provided to employees. The Florida Workers’ Compensation Act specifically lists a workers’ compensation exemption for volunteers. There are some exceptions, such as when a person is volunteering for a government entity. These volunteers are eligible for workers’ comp coverage.4

If a volunteer is eligible as an employee, they’re entitled to medical benefits. They aren’t eligible for wage loss benefits from volunteer work, however. This was decided in a 2005 court ruling when a Board of Education volunteer claimed they were entitled to weekly disability payments.5

Workers’ Compensation Classification

Companies misclassifying employees can quickly end up in lawsuits. Misclassifying an employee as an independent contractor means a business doesn’t have to withhold wages to pay taxes. The Internal Revenue Services (IRS) states employers are liable for employment taxes for misclassifying. The government agency provides small business owners with additional details to understand the differences between an employee and an independent contractor. Learn more about workers’ compensation class codes.

The Penalty for Not Having Workers’ Compensation Insurance – Different by State

Penalties differ across the U.S. because each state has its own workers' comp laws. Penalties for not carrying workers’ compensation coverage can be catastrophic for your business.

To avoid civil penalties or fines, it’s important to know what your state’s workers’ comp regulations are. Depending on the state you’re in you can obtain workers’ compensation from:

- Insurance companies or a state-run agency

- A monopolistic state agency

You can also work with an attorney to ensure you’re classifying employees correctly. Knowing the rules and working with the appropriate people can help you better understand if you or the self-employed or independent contractor needs to buy workers’ comp.

Last Updated: February 16, 2026

This article provides general information, and should not be construed as specific legal, HR, financial, insurance, tax or accounting advice. As with all matters of a legal or human resources nature, you should consult with your own legal counsel and human resources professionals. The Hartford shall not be liable for any direct, indirect, special, consequential, incidental, punitive or exemplary damages in connection with the use by you or anyone of the information provided herein.

1,2,3 New York State Workers’ Compensation Board, “Workers’ Compensation Coverage: Volunteers.”

Additional disclosures below.